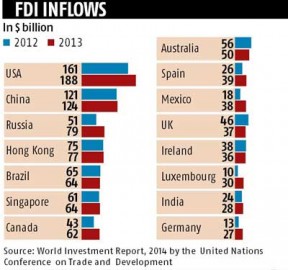

Arvind Mayaram, secretary, economic affairs, heading a panel on Friday made certain clarifications in respect to the ambiguous definition of foreign direct investment (FDI).FDI has off lately been a matter of furore in corporate labyrinth with everyone awaiting Modi government’s stand on FDI in retail. The new regulation may have an impact on the overall performance of India as a favoured FDI destination. The 2014 World Investment Report shows than India has gone down in the table of best FDI destinations in the world (see figure).

Arvind Mayaram, secretary, economic affairs, heading a panel on Friday made certain clarifications in respect to the ambiguous definition of foreign direct investment (FDI).FDI has off lately been a matter of furore in corporate labyrinth with everyone awaiting Modi government’s stand on FDI in retail. The new regulation may have an impact on the overall performance of India as a favoured FDI destination. The 2014 World Investment Report shows than India has gone down in the table of best FDI destinations in the world (see figure).

FDI pertains to international investment in which the investor obtains a lasting interest in an enterprise in another country. Most often, it may take the form of buying or constructing a factory in a foreign country or adding improvements to such a facility, in the form of property, plants or equipment.

FDI is calculated to include all kinds of capital contributions, such as the purchases of stocks, as well as the reinvestment of earnings by a wholly owned company incorporated abroad (subsidiary), and the lending of funds to a foreign subsidiary or branch. The reinvestment of earnings and transfer of assets between a parent company and its subsidiary often constitutes a significant part of FDI calculations.

Another form of overseas investment referred to as foreign portfolio investment is a category of investment instruments that is more easily traded, may be less permanent, and do not represent a controlling stake in an enterprise. These include investments via equity instruments (stocks) or debt (bonds) of a foreign enterprise which does not necessarily represent a long-term interest.

The Mayaram panel in its report suggested that foreign investment below 10% to be treated as foreign portfolio investment (involving foreign institutional investors and qualified foreign investors. Any investment of 10% or more by the overseas investor in a listed Indian company through eligible instruments will qualify as FDI. No such minimum limit has been specified in respect of unlisted companies.

The reports stated that ‘non-repatriable’ investments by non-resident Indians should be treated as domestic investment. The already existing FDI which do not meet the new suggested limit will be continued to be referred as FDI.

The panel also suggested that an investment below 10% could qualify as FDI provided that the “stake is raised to 10% or beyond within one year from the date of first purchase. The obligation to fulfill this requirement would lie on the company. If the stake is not raised in the company to 10% or beyond then it would be treated as portfolio investment”.

The recommendations of the report if accepted by the government would lead to legislative changes in the FDI rule. The rules would help bring clarity for the overseas investors in defining their investments in Indian companies as FDI or FPI and would be a deciding factor of their power in the company.

Learn more about finance and accounting outsourcing at Aristotle Consultancy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}