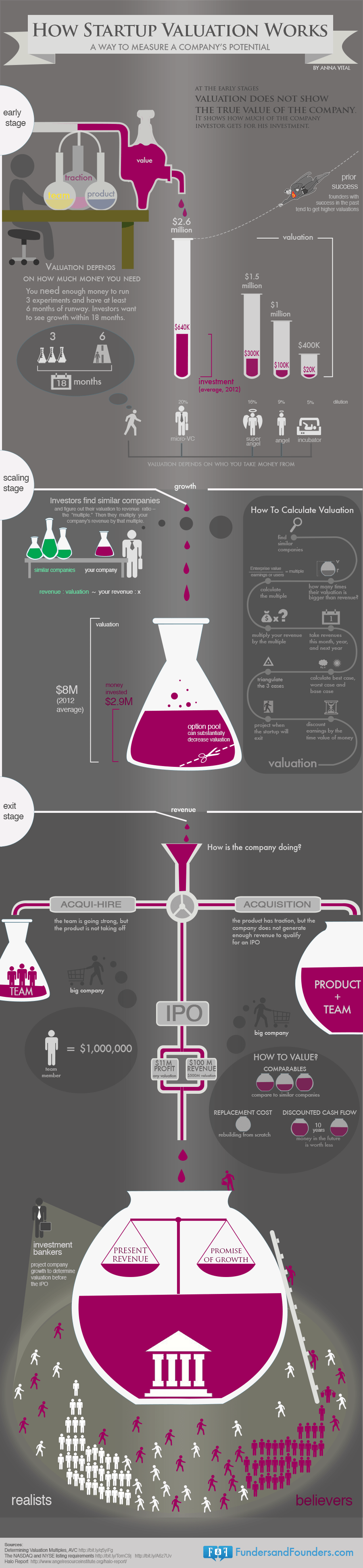

How would you measure the value of a company? Especially, a company that you started a month ago – how do you determine startup valuation? That is the question you will be asking yourself when you look for money for your company.

How do you calculate your valuation at the early stages?

1- Figure out how much money you need to grow to a point where you will show significant growth and raise the next round of investment. Let’s say that number is $100,000, to last you 18 months. Your investor does not have a lot of incentive to negotiate you down from this number. Why? Because you showed that this is the minimum amount you need to grow to the next stage. If you don’t get the money, you won’t grow – that is not in the investor’s interest. So let’s say the amount of the investment is set.

2- Now we need to figure out how much of the company to give to the investor. It could not be anything more than 50% because that will leave you, the founder, with little incentive to work hard. Also, it could not be 40% because that will leave very little equity for investors in your next round. 30% would be reasonable if you are getting a large chunk of seed money. In this case you are looking for only $100, 000, a relatively small amount. So you will probably give away 5-20% of the company, depending on your valuation.

3- As you see, $100,000 is set in stone. 5%-20% equity is also set. That puts the (pre-money) valuation somewhere between $500,000 (if you give away 20% of the company for $100,000) and $2 Million (if you give away 5% of the company for $100,000).

4- Where in that range will it be? 1.That will depend on how other investors value similar companies. 2. How well you can convince the investor that you really will grow fast.

Seed Stage

Early-stage valuation is commonly described as “an art rather than a science,” which is not helpful. Let’s make it more like a science. Let’s see what factors influence valuation.

Traction. Out of all things that you could possibly show an investor, traction is the number one thing that will convince them. The point of a company’s existence is to get users, and if the investor sees users – the proof is in the pudding.

Reputation. There is the kind of reputation that someone like Jeff Bezos has that would warrant a high valuation no matter what his next idea is. Entrepreneurs with prior exits in general also tend to get higher valuations.

Revenues. Revenues are more important for the B-to-B startups than consumer startups. Revenues make the company easier to value.

For consumer startups having a revenue might lower the valuation, even if temporarily. There is a good reason for it. If you are charging users, you are going to grow slower. Slow growth means less money over a longer period of time. Lower valuation. This might seem counter-intuitive because the existence of revenue means the startup is closer to actually making money. But startup are not only about making money, it is about growing fast while making money. If the growth is not fast, then we are looking at a traditional money-making business.

The last two will not give you an automatically high valuation, but they will help.

Distribution Channel: Even though your product might be in very early stages, you might already have a distribution channel for it.

Hotness of industry. Investors travel in packs. If something is hot, they may pay a premium

SERIES A

The main metric here is growth. How much have you grown in the last 18 months? Growth means traction. It could also mean revenue. Usually, revenue does not grow if the user base does not grow. Investors at this stage determine valuation using the multiple method, also called the comparable method, well-described by Fred Wilson. The idea is that there are companies out there similar enough to yours.

INVESTOR’S PERSPECTIVE

It is important to understand what the investor is thinking as you lay down on the table everything you have got.

1- The first point they will think is the exit – how much can this company sell for, several years from now.

2- Next they will think how much total money it will take you to grow the company to the point that someone will buy it for $1 Billion.

3- Next, the investor will figure out what percentage of that she owns. If she funded at the seed stage, let’s say 20%. (The complicated piece here is that she probably got preferred shares, which just means she gets the money before everyone else. Also, there might have been a convertible note as part of the funding, which gave her the option to buy shares later on at a set price, called “cap”.)

OTHER THINGS THAT INFLUENCE VALUATION

Option Pool. Option pool is nothing more than just stock set aside for future employees. Why do this? Because the investor and you want to make sure that there is enough incentive to attract talent to your startup. But how much do you set aside? Normally, the option pool is somewhere between 10-20%.

The bigger the option pool the lower the valuation of your startup. Why? Because option pool is value of your future employees, something you do not have yet. The options are set up so that they are granted to no one yet. And since they are carved out of the company, the value of the option pool is basically deducted from the valuation.

Learn more about accounting outsourcing at Aristotle Consultancy.

Source – fundersandfounders.com

Halo Report, NASDAQ and NYSE listing requirements, AVC – Fred Wilson’s blog, written by Anna Vital

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}